If you accept credit cards for your business, here are some helpful tips that can help you to avoid problems related to accepting and billing credit cards.

Every credit card number can be electronically checked to determine if it’s a valid number. This is helpful if you receive a credit card number from a customer, which you will be billing later. If the customer gave you the wrong number it’s very time consuming to get back in touch with the customer to get a new number. By using this checker below, you can save valuable time checking that the number is valid as soon as you receive the number. Keep in mind this only verifies that this is a valid number, not that it belongs to this particular customer or that there is adequate credit on the card. This is a useful tool to check the number while you’re taking a credit card number over the phone.

If you have a valid number but are still having problems processing the card through your merchant terminal, you might have not matched the credit card type to the number. The following information below may be useful to you.

Credit card numbers that begin with a…

3 are always American Express (AmEx)

4 are always Visa

5 are always Mastercard

6 are always Discover Card

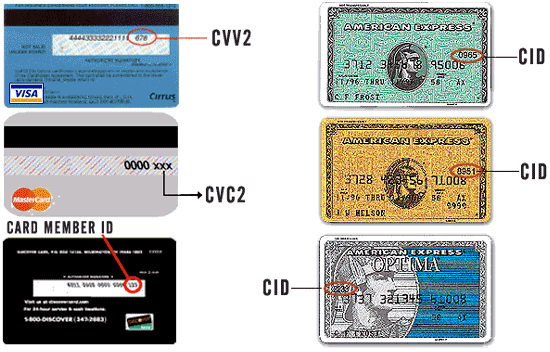

Generally you will need the CVV (this small number on the back of the card) to avoid mistakes, note that the CVV is…

3 digits on the back of the card for Visa, Mastercard and Discover Card

3 or 4 digits on the front of the card for American Express Card

CVV = Card Verification Value or Card Validation Code

CVC = Card Verification Code

CID = Card ID

Depending on the security settings on your credit card you can process a credit card based on only a subset of the 5 primary verification methods below:

Credit card number (required)

Expiration date (required)

CVV (the small 3 or 4 digit number on the back of the card)

Address (only the main digits in the address are actually checked)

Zip code

Note: all of the information used to validate a credit card are ALL NUMBERS. The credit card processor does NOT care about the spelling of the cardholder’s name, street name, city or state.

One of the most common mistakes in taking a credit card is getting the correct address. The average person has multiple credit cards and many with multiple addresses; such a credit cards for their business, with that address and others for personal use with their home address. When you receive the address information, always ask…

“Is this the address which your credit card statement is mailed to?”

More Tips & Hints

If your business only accepts physical credit cards and swipes them through a card reader for processing, then your risk of fraud is greatly reduced. Your only real issue is to make sure that the cardholder shows you a government issued photo ID and that you verify that the name on the credit card matches the name on the ID and that the picture on the ID matches the person handing you the card.

If you accept cards through a website or over the phone, life becomes much riskier. Since you don't get to see the person placing the order or physically swipe the credit card through the terminal, you have to resort to other means to minimize your risk when processing credit card transactions.

There are 2 required pieces of information and 3 optional pieces of information. The minimum information required to process a credit card transaction is the credit card number and the expiration date. If either of these are missing or wrong, the card will not be charged and the transaction will be rejected.

An additional piece of information that can be used to minimize your risk is the Card Verification Value or CVV code. This is a 3 or 4 digit (see below) number printed (NOT embossed) on the card. This means that, if a card is processed through an old machine that makes a carbon copy of the information embossed on the card, i.e. the credit card number, the expiration date and the cardholder's name, the CVV code will NOT show up on the carbon copy. Many stolen credit card numbers are obtained by going through the trash of legitimate businesses looking for discarded credit card carbon copies.

If the credit card number and the expiration date are correct AND the CVV code is missing, the credit card will still be processed and if there are sufficient funds on the card, the transaction will be approved. If the credit card number and the expiration date are correct AND the CVV code is incorrect, the credit card will NOT be processed and the transaction will be declined. If the credit card number, the expiration date AND the CVV code are all correct, and, if there are sufficient funds on the card, the transaction will be approved. This additional check will help you win a chargeback should the cardholder later dispute the transaction.

The 4th and 5th pieces of information, which are also optional, are the numeric portion of the street address and zip code of the billing address. These parameters are completely optional and you must configure your merchant account as to whether you want to accept or reject transactions with bad addresses and zips. Much like the CVV code, if the numeric portion of the billing address is correct and the cardholder later disputes the transaction, you will stand a better chance of winning the chargeback. Additionally, many merchants will only ship to the billing address to reduce fraud.

If you enable address verification and a customer enters a bad address when submitting an order, the transaction will be returned to you as a declined transaction, but the card issuing bank will show the transaction as approved. This is because, if the credit card number, expiration date and, optionally, the CVV code are correct, the card issuing bank approves the transaction. The decision to reject the transaction is made by your Internet gateway, i.e. AuthorizeNet, PayFlow, etc. The transaction will eventually be voided out at the end of the day, but in the meantime the available credit on the cardholder's account will be reduced by the amount of the transaction. If the customer makes several attempts with invalid address information, this could quickly use up all of the available credit on the cardholder's account, which will disappear the by the following day. The only workaround for this is to physically call up the cardholder's issuing bank and request that the funds be immediately released back to the cardholder. We strongly suggest that you do this if you’ve attempted to process the card more than once!

So, in summary, the CVV code is a no-brainer. You should ALWAYS require the CVV code when processing a "card not present" transaction. As for the address verification, this depends on both the average size of your transactions, your cost of goods sold and the number of transactions you process each day.